I swear I didn’t mean for it to feel like this

Like every inch of me is bruised, bruised

“Bruised”, Jack’s Mannequin

Jack’s Mannequin’s debut album Everything in Transit was released 20 years ago (this author vividly remembers finding much-anticipated leaked tracks on the depths of the internet and burning them onto CDs) and was inspired by frontman Andrew McMahon’s experience coming home after four years on the road touring with his other band, Something Corporate. The album explores the sometimes harsh reality that when you are gone, the world moves on, and people, places, and relationships change. Things are different than you remember, but you must learn to accept and adapt to your new environment.

In many ways, investors are facing a similar harsh reality of change today as they confront how different the world, markets, and policy priorities are in 2025 than they were in, say, 2017.

We have been observing just how much investors wanted this year to be a boon of positive policy drivers, with rather complacent consensus expectations for immediate beneficial offsets to detrimental policies (i.e., tax cuts to offset tariffs), an assumption that the “bark was worse than the bite” on policies like tariffs and geopolitical concerns, and even hope for a “Trump put” that would prevent any kind of market decline.

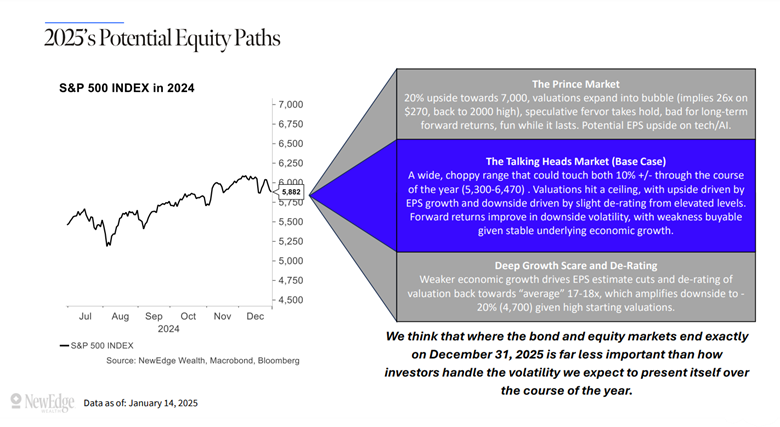

In building our 2025 equity outlook for a wide, choppy range, we added to these one-sided policy expectations observations about fulsome equity valuations, stretched positioning, and high earnings growth expectations (which also have to contemplate a meaningful deceleration in the growth rate of Magnificent 7 EPS). All these factors combine to create a higher bar for upside surprise and less cushion to absorb downside shocks, meaning upside is possible, but downside over the course of the year is likely (and a potential buying opportunity).

In the last two weeks, it is as if all these factors (policy uncertainty, mega cap earnings growth slowdown, and high valuations) have all collided, leaving equity markets feeling like Andrew McMahon returning to California: Bruised.

“There’s So Much Sun Where I’m From, I Had to Give it Away”: Set Up For Volatility

Given our expectations for a wide, choppy range in 2025, we are not all too surprised to see this bout of volatility (be it an ever so shallow -4.7% down from all-time highs).

We have been observing that for the last 6 months, the S&P 500’s price and forward earnings estimates have been diverging, meaning the last 500 pts of the S&P 500 rally (from ~5600 to ~6100) was driven entirely by multiple expansion, a more fragile set up for future gains compared to the broad support equity markets received in 2023 and 1H2024 from rising EPS estimates.

S&P 500 Price and 2025 EPS Estimate

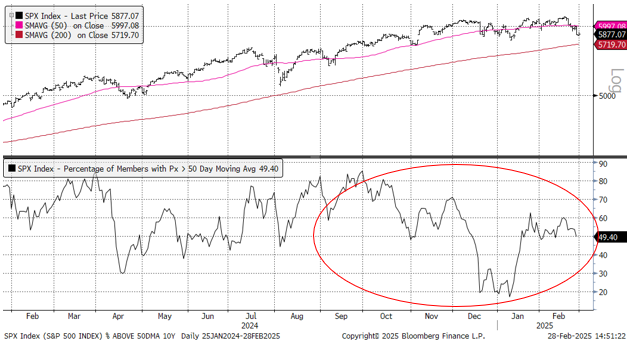

Further, we have been observing deteriorations in market momentum (weekly Moving Average Convergence Divergence (MACD) shown below) and breadth (% of names trading above their 50-day moving averages shown below). These factors are not death knells to rallies, but they suggest that a shift away from the powerful, low volatility, “up and to the right” rallies of 2023-2024 is possible. This is not to say a bear market like 2022 is imminent, but that a sideways year like 2015 and 2018 (which both included moments of incredible long-term buying opportunities) is a potential outcome for 2025.

S&P 500 with Weekly Moving Average Convergence Divergence

S&P 500 with Percentage of Members Trading Above Their 50-Day Moving Average

“Can You Make This Last?”: Magnificent 7 at Long-Term Support

From a tactical perspective, the S&P 500 is nearing an oversold level on measures like the daily Relative Strength Index, with components like the Magnificent 7 cohort already flashing an oversold condition.

The Magnificent 7 is facing a vitally important test of its longer-term, powerful uptrend, with the index of mega caps already correcting 15% to its 200-day moving average. This is partially just a reversal of the parabolic and arguably unsustainable rally that this group experienced in December’s window dressing and performance chasing, but the “gusto” of the rally coming off of this oversold condition at long-term support will be a very important tell about the ability of this cohort to remain dominant market leadership. For now, this trend deserves the benefit of the doubt, but we are watching it closely.

Bloomberg Magnificent 7 Index Absolute (Top) and Relative to the S&P 500 (Bottom)

As mentioned earlier, a big question facing the Magnificent 7 is how the market will digest 2025’s deceleration in earnings growth. According to FactSet, the cohort’s EPS is expected to go from 33% growth in 2024 to 21% growth in 2025. This contrasts with the expected acceleration in the remaining 493 EPS growth from 4% in 2024 to 11% in 2025. We remind investors that “second derivatives matter”, meaning it is the rate of change of growth that often drives prices, not the absolute level of growth.

“This Plane is All I’ve Got, So Keep it Steady Now”: Growth Fears

Another important watch item is brewing growth fears for the U.S. economy, which have been reflected in tumbling bond yields (which we previewed given weak economic surprises in late December) and the pricing in of more rate cuts for 2025. In the past few weeks, the bond market has gone from expecting just one rate cut for the year to over 2.6 cuts.

There is a growing appreciation that acute policy uncertainty and the order of policies being enacted (with the “pain” of tariffs coming long before the “gain” of tax cuts, if those are even possible given deficit concerns and slim voting majorities) are all weighing on sentiment and even business and household decision making.

Plunging consumer sentiment, an apparent peak in small business sentiment, and evidence of a pull-forward of demand to get ahead of tariffs are all reflecting this heightened policy uncertainty.

To monitor the extent of growth fears, we think it is important to keep a close eye on credit spreads to see if there is impending risk to growth estimates. High-yield credit spreads have widened over the last week but remain near multi-decade lows.

Barclay’s High Yield Spread

A continued widening of these spreads would be a sign that growth fears are becoming more pernicious and would likely coincide with a deeper equity market correction. If high yield spreads remain contained, we would expect equity weakness to remain short and shallow.

Interestingly, analysts are continuing to raise their growth estimates, mainly for household consumption, despite the recent string of weaker data. The highlighted purple line in the chart below shows how household consumption forecasts have been raised YTD, despite the ratio of equal weight Consumer Discretionary vs. Staples (a potentially helpful leading indicator of consumption forecast revisions) starting to weaken. This remains a must-watch ratio for how the equity market is judging the health of the US consumer.

Equal Weight Consumer Discretionary vs. Staples and

GDP Household Consumption Forecasts for 2023, 2024, and 2025

“I’m Here ‘Til Close With Fingers Crossed”: Conclusion

Overall, we remain long-term optimistic about U.S. equity markets, but we are not surprised to see this recent bout of volatility, mostly given the turbulent DC headlines, high starting valuations, stretched positioning, fading momentum, fading breadth, and now brewing growth fears.

Though markets might feel Bruised in the short term, we continue to see volatility as an opportunity, arguing that it is far less important where the S&P 500 ends the year and far more important what investors do with the volatility along the way.

As we enter next week, we will “lace our Chucks” in order to judge how major indices interact with support lines and bounce from oversold conditions, and we will continue to monitor credit spreads for signs that growth fears are becoming more pronounced.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC

The post Bruised appeared first on NewEdge Wealth.